I've spent the last

couple of months an investment bank in Bahrain which had (past tense)

an ambition to ally the surplus capital of the Gulf region to the

financing opportunities presented by the historic emergence of Turkey

and its near neighbours. To my mind, that was (and is) a hugely

inviting prospect. Istanbul is one of the few cities that can claim

to be the centre of the world, and right now hosts an alliance of

demographics and growth that I remember from the great Asian emerging

markets of 20 years ago. The long and short of it is that Turkey is

a country of 74+mn, with a median age of 28.5 years, a per capita

income averaging around US$10,300. Over the last decade its real GDP

growth rate has averaged 5.3%, but it's been a rough old journey,

with a standard deviation of 4.4%.

Growth, opportunity and

volatility – what's not to like for an emerging market investor?

Right now, it looks as

if 2012 will be another rocky year, with investors needing to take a

view on how far Turkey overheated last year, how quickly it is

rebalancing its economy between domestic demand and exports, and how

much appetite world markets have to keep financing Turkey's

investment spending. My sort of questions, in other words.

(Incidentally, I expect the usual suspects will markedly

underestimate the capital appetite for Turkish risk at this point:

the key datapoint being the 110% jump in FDI – the world's

stickiest money – last year).

My starting point is,

as usual, to run the Flow Essentials charts to get to the underlying

ratios Turkey's economic growth and financing depends on. Start with

estimated growth of capital stock and the direction of ROC. My

assumption is that when you've got a rapidly expanding banking system

(loan growth of 42.3% last year) you must have significant

misallocation of resources, disguised temporarily by inflation (up

6.5% on average in 2011, and rising sharply, to 10.6% YoY in

January). But even using deflated numbers, on my count capital stock

is growing around 8.6% pa (or 16.5% nominal), but ROC was no worse

than flat last year.

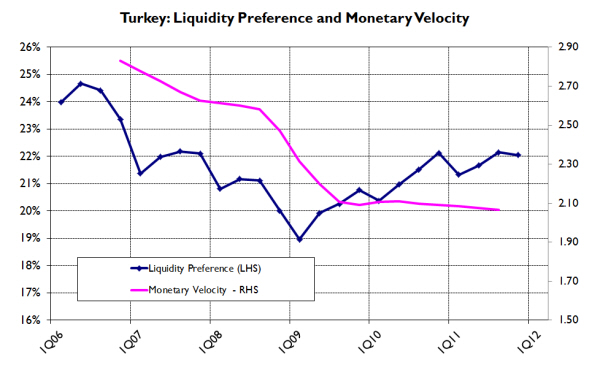

And this was borne out

by the monetary velocity reading, which again was no worse than flat.

This was a genuine

surprise: the expected misallocation should have shown up far more

starkly on these charts.

Still, leverage must

have been rising sharply, and banking data tells us that banks'

loan/deposit ratio rose from around 80% at the beginning of the year

to 89% by the end of the year, and that this had been financed at

least in part by an increase in foreign liabilities from a net

US$16.74bn at the beginning of the year to around US$20.4bn by the

end of the year. But once again, one would have expected the rise in

leverage of the banking system, and is escalating exposure to the

jitters of its foreign liabilities to be more extreme. Run the

numbers, and it turns out that only 9% of the rise in the loan book

was funded by the net increase in foreign liabilities – slightly

less than the 11.2% that was funded by banks' running down their

holdings of domestic securities.

But in the end, we

cannot escape the fact that even if Turkey's rapid 2011 growth has

been driven by rather less inefficient resource allocation than we

had expected, and even if the financing of the growth was rather less

reckless than it might have been, Turkey's growth was still powered

by a major private sector savings deficit. In fact, I estimate that

that deficit came to 9.3% of GDP in 2011.

And here is the rub:

judging how far and how fast that savings deficit is being corrected

this year is surely the key to potentially one of the most exciting

turnaround stories of the year. More, much more, to follow. . . .